Julia's Blog

Julia's Blog

Tax Treatment of Electric Vehicles

There has been a lot of talk about the FBT concessions associated with electric cars, this blog explains the latest on that from an employee and an employer’s point of view. Let’s start with an area that does not seem to be getting any publicity, deductions for the employer who charges the car at home.

Claiming Electricity for Charging an EV at Home

As an employee who is charging your employer provided EV at your home you can claim the electricity used as a tax deduction. The idea would be to turn off everything else in the house and just run the charger then look at the metre box to see how much it uses. Your electricity bill will give you the information on the cost per hour of that amount of usage. From there you just need to record how many hours it is charging and multiply it by that rate. The calculation together with a diary for one month each year of the hours charging will satisfy the ATO.

If you, not your employer, own the EV and you are using the log book method to apportion the deductible percentage then you should also record the electricity used in charging the EV and include it in the other vehicle expenses that are apportioned to work out your tax deduction.

What about the cost of installing the charger? Unfortunately, this is part of the building not actually plant and equipment so no deduction or depreciation for that expense.

The FBT Concession:

There is no Fringe Benefits Tax payable on electric vehicles for at least the first 3 years. As a general rule of thumb the FBT on a car is normally round 20% of the purchase price of the vehicle, payable each year until the vehicle has been held for at least 4 full FBT years when it reduces to 2/3rds of 20%. Over the 3 years that is 60% of your purchase price. This is a huge saving to your salary package or your business. It means not only does your employer get the GST back on the purchase price and ongoing expenses but even though there is private use of the vehicle the expenses are effectively paid out of before tax dollars.

The Immediate Write off:

If you are a small business, you can claim a full tax deduction for any plant and equipment you buy for your business, as long as it is installed ready for use by 30th June, 2023. Having said that, when it comes to cars there is a cap which is discussed below under the heading of Luxury Car Limit.

The immediate write off concessions will not work for a novated lease arrangement or for any lease arrangement for that matter because the vehicle is simply rented, not purchased. This causes a problem when the employee wants to effectively own the car but have their employer make the lease payments in order to get the GST back and have the motor vehicle expenses effectively paid out of before tax dollars.

The immediate write off provides quite an incentive for the employer to own the vehicle, that is assuming the employer has a tax problem. It also provides an incentive to purchase your car and have it installed ready for use before 30th June 2023, good luck with that one.

The Luxury Car Limit off:

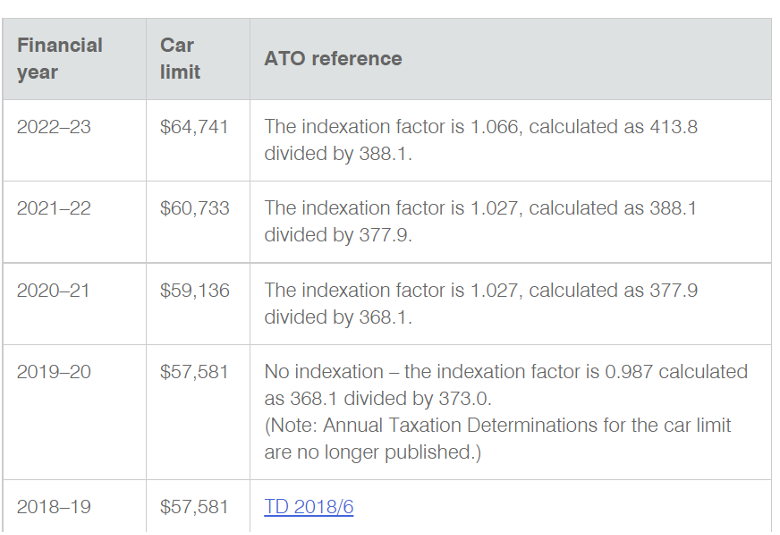

The concession only applies to electric cars that are under the luxury car limit which is:

It is important to note there is a difference between the luxury car tax threshold in the table above and car limit for depreciation purposes in the table below. You will qualify for the FBT concession if your car is under the luxury car tax threshold but you will not be able to depreciate or immediately write off all of its value unless it is also under the car limit for depreciation, below.

So if you wait until after the 30th June, 2023 you have a better chance of the price coming under these limits but you will miss out on the immediate write off. Note the immediate write off is not always a sensible move, the depreciation deduction maybe more valuable to you in future years, claimed as a lump sum it may reduce you down to only the 19% tax rate, wasting future tax deductions. On the other hand prices of electric cars may go up just as much as the thresholds do anyway.

Note the thresholds above apply to cars, so if the vehicle you are buying is a non car for example a vehicle designed to carry more than 1 tonne then there is no limit. An interesting tip in this regard is the threshold is measured against only the purchase price, only the first element. Once you have the vehicle in use you can further modify it and even though that extra cost may take it over the threshold, it does not matter, as long as the original purchase price is under the limit.

The flip side of this is, once a car always a car. So if you buy a car and modify it to the extent that it is a non car it won’t change it from being treated as a car for the depreciation limit. Though if the modifications are done after it is installed ready for use then they are depreciated or written off separately so not capped.

Here are some of the specifics from the bill:

| Low and zero emission cars |

|

| The car was first held and used on or after 1 July 2022 | Where the car is first held and used on or after 1 July 2022. Provided the conditions of the exemption are met, an electric car that was ordered prior to 1 July 2022, but was not delivered until after 1 July 2022 would be eligible for the exemption (even if an employer acquired legal title to the car before 1 July 2022). However, a car delivered to you prior to 1 July 2022 would not qualify. A second-hand electric car may qualify for the exemption, provided that the car was first purchased new on or after 1 July 2022. |

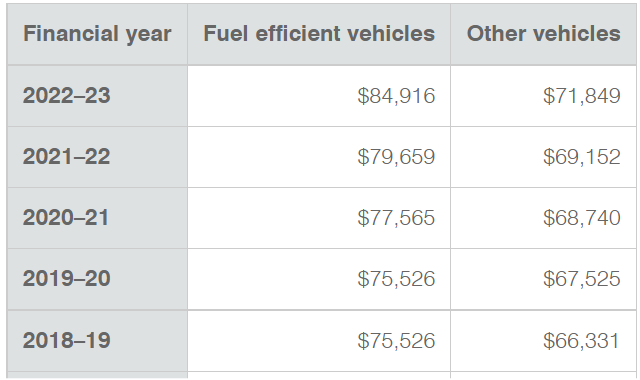

| Value below luxury car tax threshold for fuel efficient vehicles | The value of the car at the first retail sale must be below the luxury car tax threshold ($84,916 in 2022-23) for fuel efficient vehicles. The luxury car tax threshold generally includes GST and customs duty but excludes other items such as service plans, extended warranties, stamp duty and registration. |

EV State and Territory tax concessions

ACT

The ACT Government offers a stamp duty exemption on new zero emission vehicles, and up to two years free registration for new or second hand zero emission vehicles (registered between 24 May 2021 and before 30 June 2024).

New South Wales

Reimbursement of stamp duty paid on purchases of new or used full battery electric vehicles (BEVs) and hydrogen fuel cell electric vehicles (FCEVs), with a dutiable value up to and including $78,000.

Northern Territory

For plug-in electric vehicles (battery and hybrid plug-in), from 1 July 2022 until 30 June 2027, access free registration for new and existing vehicles and a stamp duty concession of up to $1,500 on the first $50,000 of the car’s market/sale value – 3% thereafter.

Queensland

Discounted registration duty for hybrid and electric vehicles. And, a limited $3,000 rebate for new eligible zero emission vehicles with a purchase price (dutiable value) of up to $58,000 (including GST) on or after 16 March 2022.

South Australia

A limited $3,000 subsidy and a 3-year registration exemption on eligible new battery electric and hydrogen fuel cell vehicles first registered from 28 October 2021.

Tasmania

From 1 July 2022 until 30 June 2022, no stamp duty applies to light electric or hydrogen fuel-cell motor vehicle (including motorcycles). Vehicles with an internal combustion engine do not qualify.

Victoria

A limited $3,000 subsidy is available for new eligible zero emission vehicles purchased on or after 2 May 2021. More than 20,000 subsidies are available under the program. Plus, stamp duty for ‘green passenger cars’ is set at the one rate regardless of value ($8.40 per $200 or part thereof). Zero emission vehicles receive a $100 annual registration concession but are also subject to a per kilometre road user charge.

Western Australia

A $3,500 rebate on the purchase of a new zero emission, hydrogen fuel cell or battery light vehicle with a value of up to $70,000 purchased on or after 10 May 2022.